All Categories

Featured

Table of Contents

At the end of the day you are buying an insurance coverage item. We love the defense that insurance coverage uses, which can be acquired much less expensively from a low-cost term life insurance policy policy. Unpaid loans from the policy might also lower your survivor benefit, diminishing an additional degree of defense in the policy.

The concept only works when you not just pay the substantial premiums, yet make use of extra cash money to purchase paid-up enhancements. The chance price of every one of those dollars is significant very so when you can instead be buying a Roth IRA, HSA, or 401(k). Even when compared to a taxed financial investment account or perhaps an interest-bearing account, boundless financial might not use similar returns (contrasted to spending) and similar liquidity, access, and low/no cost framework (compared to a high-yield interest-bearing accounts).

When it comes to economic preparation, entire life insurance policy often stands apart as a prominent option. There's been an expanding fad of advertising and marketing it as a device for "boundless banking." If you've been exploring entire life insurance policy or have actually stumbled upon this principle, you could have been told that it can be a way to "become your very own bank." While the concept may sound attractive, it's vital to dig much deeper to understand what this actually suggests and why viewing entire life insurance policy by doing this can be misleading.

The concept of "being your own bank" is appealing because it recommends a high level of control over your funds. Nonetheless, this control can be imaginary. Insurance policy companies have the ultimate say in just how your plan is handled, including the terms of the lendings and the rates of return on your cash money value.

If you're thinking about whole life insurance, it's vital to watch it in a more comprehensive context. Whole life insurance policy can be an important tool for estate planning, supplying a guaranteed survivor benefit to your recipients and potentially offering tax advantages. It can also be a forced financial savings automobile for those who have a hard time to save cash constantly.

It's a form of insurance policy with a financial savings element. While it can supply constant, low-risk growth of cash money worth, the returns are usually reduced than what you may achieve through various other financial investment cars (my wallet be your own bank). Prior to leaping right into whole life insurance policy with the idea of unlimited banking in mind, make the effort to consider your monetary goals, danger tolerance, and the complete variety of economic products offered to you

Direct Recognition Whole Life

Boundless financial is not an economic remedy. While it can function in particular scenarios, it's not without dangers, and it calls for a considerable dedication and comprehending to handle effectively. By identifying the possible mistakes and comprehending real nature of entire life insurance policy, you'll be much better geared up to make an enlightened choice that sustains your monetary wellness.

This book will educate you exactly how to establish a banking plan and how to make use of the banking policy to buy realty.

Boundless banking is not an item or solution provided by a particular organization. Limitless banking is a strategy in which you buy a life insurance policy policy that builds up interest-earning cash money value and obtain finances versus it, "obtaining from on your own" as a source of funding. Ultimately pay back the car loan and start the cycle all over once more.

Pay policy premiums, a portion of which constructs cash money worth. Take a loan out against the plan's cash money value, tax-free. If you utilize this idea as intended, you're taking cash out of your life insurance coverage policy to buy whatever you 'd need for the remainder of your life.

The are entire life insurance and global life insurance policy. grows money value at an ensured rates of interest and likewise through non-guaranteed returns. expands money worth at a taken care of or variable rate, depending on the insurance firm and policy terms. The cash value is not added to the survivor benefit. Money worth is an attribute you take advantage of while alive.

The policy financing interest rate is 6%. Going this course, the passion he pays goes back into his policy's cash worth rather of a monetary institution.

Become Your Own Bank Whole Life Insurance

Nash was a financing specialist and follower of the Austrian college of business economics, which promotes that the value of products aren't clearly the result of conventional economic structures like supply and demand. Instead, individuals value money and items in a different way based on their economic standing and requirements.

Among the pitfalls of typical banking, according to Nash, was high-interest rates on lendings. Way too many individuals, himself consisted of, got right into financial trouble because of reliance on financial organizations. Long as financial institutions established the passion prices and loan terms, people really did not have control over their own wide range. Becoming your very own lender, Nash figured out, would certainly put you in control over your monetary future.

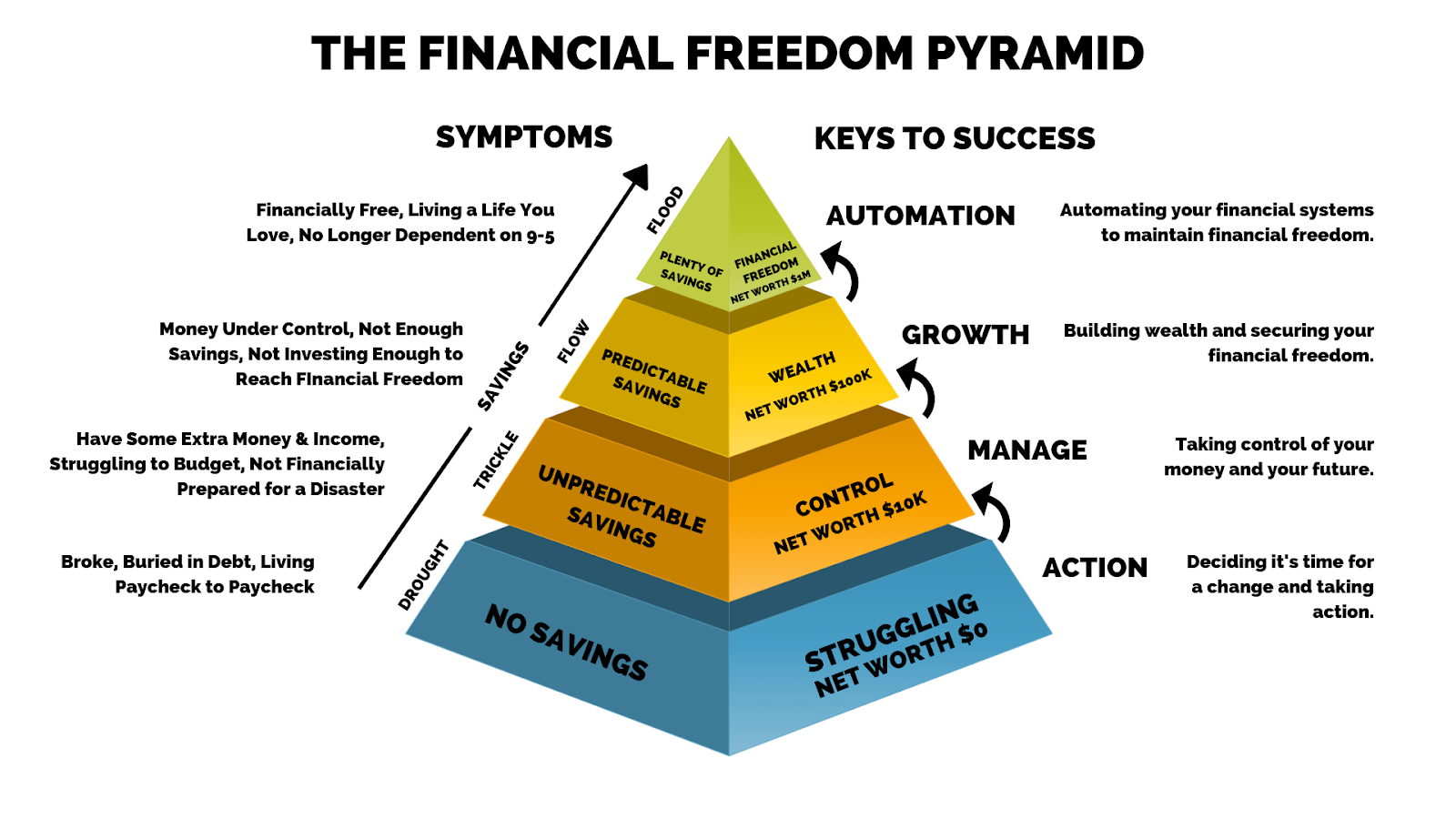

Infinite Banking needs you to own your economic future. For goal-oriented individuals, it can be the finest economic device ever before. Below are the advantages of Infinite Banking: Arguably the single most useful facet of Infinite Financial is that it enhances your money flow.

Dividend-paying entire life insurance policy is very reduced danger and provides you, the insurance holder, a large amount of control. The control that Infinite Banking offers can best be grouped into 2 classifications: tax advantages and possession securities. One of the factors entire life insurance policy is suitable for Infinite Banking is just how it's taxed.

When you utilize whole life insurance coverage for Infinite Financial, you enter into a private agreement between you and your insurance firm. These protections might differ from state to state, they can include defense from property searches and seizures, defense from judgements and defense from creditors.

Whole life insurance policy policies are non-correlated properties. This is why they function so well as the economic structure of Infinite Financial. No matter what takes place on the market (stock, actual estate, or otherwise), your insurance plan maintains its worth. Way too many individuals are missing out on this vital volatility barrier that assists protect and expand wide range, rather dividing their cash right into two containers: bank accounts and financial investments.

Infinite Banking Concept Wikipedia

Whole life insurance is that 3rd pail. Not only is the price of return on your entire life insurance coverage policy ensured, your fatality benefit and costs are additionally ensured.

Below are its main advantages: Liquidity and access: Plan lendings offer immediate accessibility to funds without the limitations of traditional financial institution finances. Tax obligation effectiveness: The cash money value expands tax-deferred, and plan finances are tax-free, making it a tax-efficient tool for developing wide range.

Asset defense: In several states, the money value of life insurance policy is protected from creditors, adding an additional layer of monetary security. While Infinite Banking has its values, it isn't a one-size-fits-all option, and it comes with considerable downsides. Right here's why it might not be the most effective technique: Infinite Financial often calls for complex plan structuring, which can puzzle insurance policy holders.

Visualize never ever having to fret concerning bank financings or high interest prices again. That's the power of unlimited financial life insurance coverage.

There's no set car loan term, and you have the flexibility to select the repayment schedule, which can be as leisurely as settling the car loan at the time of fatality. This flexibility encompasses the maintenance of the fundings, where you can go with interest-only payments, keeping the loan balance level and workable.

Holding cash in an IUL dealt with account being attributed passion can commonly be better than holding the money on deposit at a bank.: You've constantly fantasized of opening your very own bakeshop. You can obtain from your IUL plan to cover the initial costs of leasing an area, purchasing equipment, and employing team.

Rbc Royal Bank Visa Infinite Avion

Individual fundings can be obtained from typical banks and credit rating unions. Here are some bottom lines to consider. Charge card can supply a flexible way to borrow cash for very short-term durations. Nevertheless, borrowing money on a charge card is usually extremely expensive with yearly portion rates of rate of interest (APR) often getting to 20% to 30% or even more a year.

The tax obligation treatment of plan financings can vary significantly relying on your country of residence and the particular terms of your IUL plan. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, policy financings are usually tax-free, using a significant advantage. Nevertheless, in various other jurisdictions, there might be tax implications to think about, such as possible taxes on the car loan.

Term life insurance policy just gives a death benefit, without any cash money value build-up. This implies there's no money worth to obtain against.

However, for financing officers, the substantial regulations imposed by the CFPB can be seen as troublesome and restrictive. Car loan police officers usually suggest that the CFPB's policies create unneeded red tape, leading to even more paperwork and slower lending handling. Policies like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) requirements, while targeted at safeguarding consumers, can result in hold-ups in closing bargains and increased operational prices.

{kind=link}

Latest Posts

Whole Life Insurance-be Your Own Bank : R/personalfinance

Can I Be My Own Bank

How To Become My Own Bank