All Categories

Featured

Table of Contents

Okay, to be reasonable you're really "financial with an insurance provider" instead of "financial on yourself", yet that idea is not as easy to offer. Why the term "boundless" financial? The concept is to have your cash working in multiple places at when, instead of in a solitary location. It's a bit like the concept of getting a residence with cash money, after that borrowing versus your house and putting the cash to function in one more financial investment.

Some individuals like to speak about the "speed of money", which generally implies the very same point. In reality, you are simply making best use of utilize, which functions, yet, certainly, works both methods. Frankly, every one of these terms are rip-offs, as you will certainly see listed below. But that does not suggest there is nothing worthwhile to this concept once you surpass the advertising.

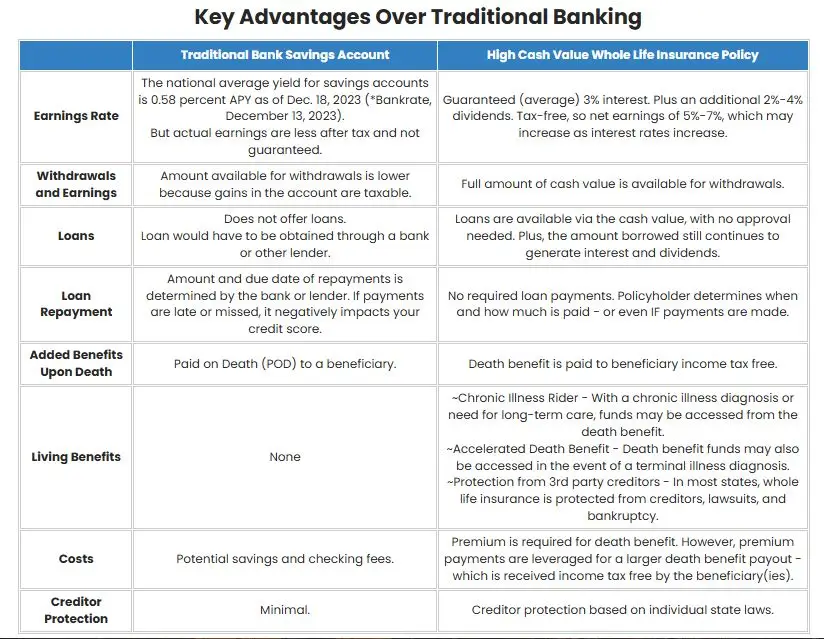

The entire life insurance industry is plagued by extremely expensive insurance, large commissions, dubious sales techniques, reduced rates of return, and improperly educated customers and salespeople. Yet if you desire to "Rely on Yourself", you're going to have to fall to this sector and actually purchase whole life insurance. There is no substitute.

The assurances intrinsic in this product are important to its feature. You can borrow against many sorts of cash value life insurance policy, but you shouldn't "bank" with them. As you acquire an entire life insurance policy plan to "financial institution" with, bear in mind that this is an entirely separate area of your financial plan from the life insurance policy area.

As you will certainly see below, your "Infinite Banking" plan really is not going to reliably provide this essential monetary feature. An additional issue with the truth that IB/BOY/LEAP counts, at its core, on a whole life policy is that it can make buying a policy bothersome for several of those interested in doing so.

Infinite Banking Center

Dangerous hobbies such as SCUBA diving, rock climbing, skydiving, or flying additionally do not blend well with life insurance policy items. That may work out fine, since the factor of the policy is not the fatality benefit, however remember that acquiring a plan on small children is more costly than it must be given that they are usually underwritten at a "common" rate rather than a preferred one.

The majority of plans are structured to do either things. Most frequently, policies are structured to optimize the payment to the representative selling it. Cynical? Yes. Yet it's the reality. The commission on an entire life insurance policy plan is 50-110% of the initial year's costs. Occasionally plans are structured to optimize the survivor benefit for the premiums paid.

The price of return on the policy is extremely crucial. One of the finest means to optimize that factor is to get as much cash money as possible into the policy.

The best method to enhance the rate of return of a plan is to have a reasonably tiny "base plan", and after that put more money into it with "paid-up additions". With more cash in the plan, there is more cash worth left after the costs of the fatality benefit are paid.

A fringe benefit of a paid-up enhancement over a routine premium is that the compensation rate is lower (like 3-4% instead of 50-110%) on paid-up additions than the base policy. The much less you pay in payment, the greater your price of return. The rate of return on your cash value is still mosting likely to be adverse for some time, like all money value insurance plan.

It is not interest-free. As a matter of fact, it might cost as much as 8%. Many insurance provider just use "straight acknowledgment" financings. With a straight acknowledgment financing, if you borrow out $50K, the dividend price related to the cash money value yearly just uses to the $150K left in the policy.

How To Start Infinite Banking

With a non-direct acknowledgment loan, the company still pays the very same reward, whether you have actually "obtained the cash out" (practically against) the plan or otherwise. Crazy, right? Why would certainly they do that? Who knows? They do. Commonly this feature is coupled with some much less helpful aspect of the plan, such as a lower dividend rate than you may obtain from a policy with straight recognition finances (benefits of infinite banking).

The business do not have a source of magic free money, so what they give in one area in the policy must be drawn from one more location. But if it is drawn from an attribute you care much less around and place right into a function you care more about, that is a good point for you.

There is another critical attribute, generally called "laundry fundings". While it is fantastic to still have actually dividends paid on money you have taken out of the policy, you still need to pay interest on that loan. If the dividend rate is 4% and the finance is billing 8%, you're not precisely coming out ahead.

With a wash car loan, your finance rate of interest coincides as the returns price on the plan. While you are paying 5% passion on the finance, that interest is completely balanced out by the 5% dividend on the financing. In that regard, it acts just like you withdrew the cash from a financial institution account.

5%-5% = 0%-0%. Without all three of these factors, this policy simply is not going to work really well for IB/BOY/LEAP. Nearly all of them stand to profit from you purchasing right into this concept.

There are lots of insurance coverage representatives chatting about IB/BOY/LEAP as a feature of entire life who are not really selling policies with the essential functions to do it! The problem is that those who recognize the idea best have a massive problem of rate of interest and generally blow up the advantages of the principle (and the underlying policy).

How Does Infinite Banking Work

You ought to contrast loaning against your policy to taking out cash from your financial savings account. No cash in cash worth life insurance coverage. You can put the cash in the bank, you can invest it, or you can buy an IB/BOY/LEAP plan.

It expands as the account pays interest. You pay taxes on the rate of interest every year. When it comes time to get the boat, you take out the cash and buy the boat. Then you can conserve some more cash and put it back in the financial account to begin to gain interest once again.

When it comes time to acquire the watercraft, you sell the financial investment and pay taxes on your long term capital gains. You can conserve some more cash and purchase some even more financial investments.

The cash money worth not made use of to spend for insurance coverage and commissions grows for many years at the dividend price without tax drag. It begins out with negative returns, however ideally by year 5 or so has actually broken also and is expanding at the reward rate. When you most likely to buy the watercraft, you obtain against the plan tax-free.

Nash Infinite Banking

As you pay it back, the cash you paid back begins growing again at the dividend rate. Those all work pretty likewise and you can contrast the after-tax prices of return. The fourth alternative, however, functions very differently. You do not save any type of money nor acquire any kind of kind of investment for several years.

They run your credit and offer you a funding. You pay rate of interest on the obtained money to the bank till the lending is repaid. When it is repaid, you have an almost pointless boat and no money. As you can see, that is nothing like the first three choices.

{kind=link}

Latest Posts

Whole Life Insurance-be Your Own Bank : R/personalfinance

Can I Be My Own Bank

How To Become My Own Bank